Frequently Asked Questions

Keith Uthe Demystifying Mortgages

What are the Benefits of a Mortgage Broker?

What is the Difference Between Fixed & Variable Rate Mortgages?

Mortgage Renewal FAQs: What Homeowners Need to Know

What is a mortgage?

A mortgage is a loan provided by a financial institution to help individuals or families purchase a property. It is secured by the property itself, and the borrower makes regular payments (including principal and interest) over a predetermined period until the loan is fully repaid.

How does the mortgage pre-approval process work?

During the mortgage pre-approval process, a lender evaluates your financial situation, including your credit score, income, and debts, to determine how much they are willing to lend you. This gives you an estimate of your borrowing capacity and can help you in your home search. Pre-approvals are typically valid for a certain period, usually around 90 days.

What is mortgage default insurance, and when is it required?

Mortgage default insurance, also known as mortgage insurance, is required for homebuyers with a down payment of less than 20% of the purchase price. This insurance protects the lender in case the borrower defaults on the mortgage. It is provided by mortgage insurance providers like Canada Mortgage and Housing Corporation (CMHC) or Genworth Canada.

What is a mortgage term, and how does it affect my mortgage?

A mortgage term refers to the length of time you commit to a specific mortgage agreement with a lender. It can range from 1 to 10 years in Canada. During the term, you will have a set interest rate and specific conditions. At the end of the term, you can choose to renew your mortgage, negotiate new terms, or pay off the remaining balance.

What is the difference between a fixed-rate and a variable-rate mortgage?

A fixed-rate mortgage has an interest rate that remains constant throughout the term, providing predictable monthly payments. On the other hand, a variable-rate mortgage has an interest rate that can fluctuate with changes in the prime lending rate, potentially affecting your monthly payments.

What is a mortgage down payment, and how much do I need?

A mortgage down payment is the initial amount you pay towards the purchase price of a property. The minimum down payment requirement in Canada is 5% of the purchase price for properties up to $500,000. For properties above $500,000, a 10% down payment is required on the portion exceeding $500,000. A higher down payment can reduce the amount you need to borrow and may affect mortgage insurance requirements.

What are closing costs, and what should I expect?

Closing costs are additional expenses associated with finalizing the purchase of a property and securing a mortgage. They can include legal fees, home appraisal fees, land transfer taxes, title insurance, and other administrative costs. It is important to budget for these costs, as they typically range from 1.5% to 4% of the purchase price.

What is mortgage prepayment, and can I make extra payments towards my mortgage?

Mortgage prepayment refers to making additional payments towards your mortgage principal, either through lump-sum payments or increasing your regular payment amount. Many mortgages allow for prepayment privileges, which can help you pay off your mortgage faster and potentially save on interest costs. However, specific prepayment options can vary, so it's essential to review your mortgage terms or consult with your lender.

Can I transfer my mortgage to another lender?

Yes, it is possible to transfer your mortgage to another lender. This is known as mortgage refinancing or mortgage portability. By transferring your mortgage, you may be able to take advantage of better interest rates, terms, or features offered by another lender. However, there may be costs associated with transferring, such as discharge fees or legal fees, so it's essential to consider these factors before making a decision.

What is the difference between going to my bank and using a mortgage broker?

The difference lies in the options and convenience. When you go to your bank, you are limited to their mortgage products. In contrast, a mortgage broker offers access to various lenders and can find the best mortgage solution tailored to your needs. They can negotiate better rates and terms and provide unbiased advice. Ultimately, a mortgage broker gives you more choice and saves you time and effort in finding the right mortgage.

Does the bank have to offer you a mortgage renewal?

No, your lender is not obligated to renew your mortgage. While most lenders do offer a renewal, they can decline if your financial situation has changed. This is why it's important to review your options and speak with a mortgage professional before your renewal date.

What happens if I'm behind on payments at the time of renewal?

If you are behind on payments, your lender may be less likely to renew your mortgage under favorable terms—or at all. However, you still have options. A mortgage broker can help you explore alternative lenders or restructuring solutions to avoid default.

Can I switch lenders at the time of my mortgage renewal?

Yes, mortgage renewal is one of the best times to switch lenders. You can shop around for better rates, terms, and flexibility. In many cases, switching lenders can help you save money or access better mortgage features.

Do I need to requalify if I switch lenders at renewal?

Yes, switching lenders typically requires requalification, including income verification, credit check, and possibly a home appraisal. However, the benefits often outweigh the process if you secure a better rate or structure.

Can I access equity in my home at mortgage renewal?

Yes, renewal is a great opportunity to access your home equity. You may be able to refinance your mortgage or set up a home equity line of credit (HELOC) to fund renovations, consolidate debt, or invest.

Is it better to renew or refinance my mortgage?

It depends on your financial goals. A standard renewal keeps your current balance, while refinancing allows you to restructure your mortgage, access equity, or consolidate debt. A professional can help determine the best option for your situation.

Can I negotiate my mortgage renewal rate?

Absolutely. You are not obligated to accept your lender

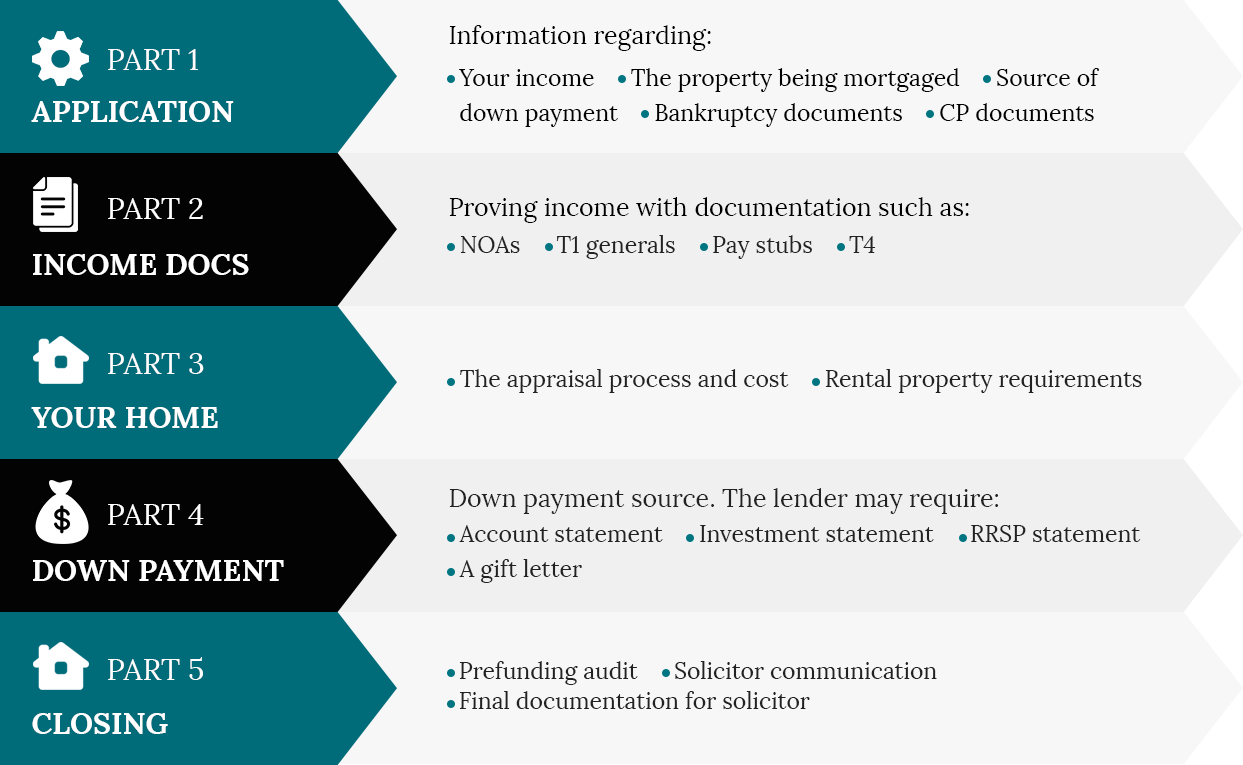

What is the Mortgage Process?